- Share

Anna J.

Marketing Intern

11 October 2022, 14:45

Tagline

Marketing Intern

11 October 2022, 14:45

Tagline

Customer screening is the process of dynamically comparing the data you have about your customers with data from external data sources such as sanctions lists, watch lists, PEP lists, and negative news.

Customer Screening & Customer Risk Rating is an important step to perform a risk-based approach. Therefore, licensed financial institutions, DNFBPs, and VASPs must undertake regular & ongoing screening.

The purpose of customer screening is to identify customer risks through a risk assessment. The procedures used for this purpose are called “Know Your Customer” and “Customer Due Diligence” procedures.

In the “Know Your Customer” (KYC) procedures, customer information is collected and its accuracy is verified. After confirming the accuracy of the customer information, customer due diligence procedures are put in place. That covers the PEP and sanction checks which will be explained on a later stage.

Customer Risk Screening is important to minimize your company’s exposure to, for example, money laundering and terrorist financing. The focus is therefore on managing the risk of doing business with “bad actors” such as sanctioned or wanted persons and identifying customers or potential customers who pose an increased risk of crime. This is because it is the only way to take appropriate measures to manage the risk, such as applying enhanced due diligence.

In addition, customer screening is required by anti-money laundering (AML) laws in most countries. Regulators and international organizations such as the Financial Actions Task Force (FATF) are pushing for proper screening techniques.

Failure to verify your customers can have numerous consequences for your business, from fines and reputational damage to criminal prosecution of employees and directors.

High-risk customers can also damage the company’s reputation. This is because others may attribute little prudence and reliability to the company as a result. Especially when particularly negative incidents are discussed in the press.

The last aspect is the relevance of effective customer screening.

The onboarding process is critical for companies in terms of customer experience. Companies want their customers to experience a fast and seamless onboarding process. And that is only possible with effective customer screening. After all, if the customer check takes days at the beginning of the relationship and customers can’t access the product or service until that late, it reduces the customer experience.

It is therefore relevant to carry out customer screening as quickly as possible.

The (types of) companies that are legally required to perform customer screening differ from country to country. In almost all countries, there is an “AML-regulated sector”. All businesses that fall within this sector are required to perform screening as part of their KYC obligations.

In general, it is not only banks that are obliged to perform customer screening. They include a variety of other financial industry organizations, such as:

However, DNFBPs can also be required to perform the client check. These include, for example:

Overall, it can be said: If there is a possibility of money laundering, tax evasion or financing of crime in the day-to-day operations of the entity, the organization and its employees must be aware of the rules and regulations for customer risk.

If you are unsure whether your company is required to conduct AML customer screening, your trade association or trade body can clarify the rules that apply to you. Screening is also commonly used by companies that are not subject to AML regulation to protect against the risk of reputational damage when doing business with certain customers. Furthermore, to manage the risk from, for example, bribery and corruption, a problem that is particularly acute in the commodities, defense and pharmaceutical industries.

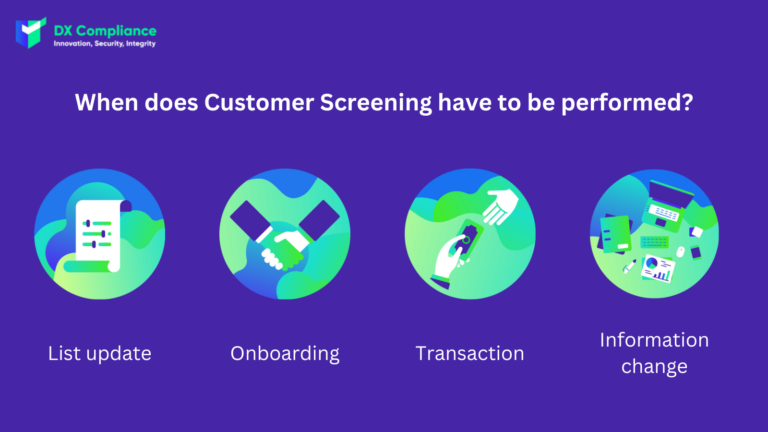

According to the latest guidance, customer risk screening must be undertaken in the following:

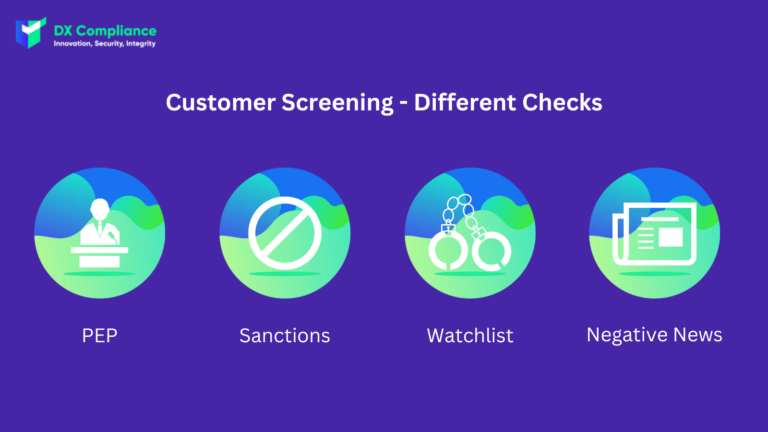

When asking how customer screening is performed, the first question to be answered is what exactly is being checked.

Politically exposed persons (PEPs) are persons who hold or have held an important public function. This function may, for example, give them influence over the use of taxpayer funds or the awarding of contracts by state-owned enterprises. As such, they are considered by the Financial Action Task Force to be a category of individuals more vulnerable to bribery, corruption, and money laundering than most.

> Learn more about politically exposed persons

Individual countries and multinational organizations (e.g., the EU and the United Nations) impose sanctions to pressure other countries or organizations to change their behavior. Sanctions can be directed against individuals, specific companies, or entire nations.

There are 2 main types of financial sanctions: Asset freezing and the prohibition to offer funds and services.

> Learn more about sanction screening

Watch lists/blacklists include natural and legal persons who pose an increased risk of financial crime due to their past behavior. These include, for example, wanted criminals or individuals who are prohibited from holding directorships or executive positions in the financial industry.

Negative news screening is the monitoring of information (called negative news) from customers or business partners in order to integrate it into risk management. In other words, deriving risks from the information.

For example, a review might reveal that a potential customer has been convicted of a crime but is not considered sufficiently relevant to financial crimes to be included on a watch list.

As the term suggests, customer creening focuses on the customer or potential customer. But this need not or should not be the only focus. There are a large number of other actors for whom a check makes sense in order to minimize the company’s own risk.

Thus, the following databases should be included in the screening process:

For higher risks, take appropriate measures to manage and mitigate the risks. They should also undertake additional and enhanced screening measures (such as negative news screening).

For lower risks, you should ensure that the screening measures are appropriate to the lower risk. They must ensure the full implementation of targeted financial sanctions in each risk scenario.

DX Compliance is an AML and Compliance firm helping our clients identify, prevent and report financial crime. DX Compliance help Banks, FinTech’s and Payments Providers to continually monitor their risk and detect the threat of money laundering to ensure compliance and reduce fines.

DX Compliance offers two products to support our Clients in the UAE and beyond. A world class real-time AI Transactions Monitoring Platform and an instant AML Check Platform called CheckAML.

Our automated customer screening solution within the transaction monitoring performs the checks on 3 levels without any manual activity: The onboarding (new customers), ongoing (daily) and transactional. You achieve risk minimization through regular risk assessments.

Furthermore, CheckAML is our ad-hoc PEP and Sanctions & Risk Analysis check tool which can be used for doing Ad-hoc checks on potential clients. That means that it only takes a few seconds to check the risk of a person or organization.

Curious? Please contact our experts!

08.08.2022

An overview of recent AML developments in the UAE.

Get access

15.10.2021

The introduction of 6AMLD regulations aims to reduce financial crimes.

Get access

27.07.2021 AML Compliance

Uncovering the PEP and Sanctions Lists and Global Regulation

Get access